Ambuja Cements Q2 FY26 results| Ambuja Cements profit| Adani Group cement| Ambuja Cements revenue| cement stocks India| Ambuja Cements expansion| Indian stock market results| NSE BSE earnings| Adani Cement

Ambuja Cements Limited, part of the Adani Group, has delivered a remarkable performance for the quarter ended September 30, 2025 (Q2 FY26). The company reported a consolidated net profit of ₹1,766 crore, marking a 268% year-on-year (YoY) surge, driven by robust volume growth, improved realizations, and operational efficiency gains. Revenue rose by 25% to ₹9,174 crore from ₹7,330 crore in the same quarter last year.

This quarter marks Ambuja’s highest-ever quarterly volume performance, highlighting the company’s strong position in India’s cement sector and its rapid capacity expansion under the Adani Group’s leadership.

Key Financial Highlights (Ambuja Cements Q2 FY26 Results)

- Revenue from Operations: ₹9,174 crore (↑ 25% YoY)

- EBITDA: ₹1,761 crore (↑ 58% YoY)

- EBITDA Margin: 19.2%

- Net Profit: ₹1,766 crore (↑ 268% YoY)

- EPS (Earnings per Share): ₹7.2 per share

- Sales Volume: 16.6 million tonnes (↑ 20% YoY)

- EBITDA per tonne: ₹1,060 (vs ₹803 per tonne last year)

- Net Worth: ₹69,493 crore

- Debt Position: Remains debt-free with a strong AAA (Stable) credit rating

The strong performance reflects Ambuja’s ability to control costs, improve efficiency, and capture increased demand across India’s infrastructure and housing segments.

Management Commentary

Ambuja Cements’ management emphasized that the quarter’s performance demonstrates the success of the company’s “lean, green, and digital” growth strategy. Under the Adani Group, Ambuja has been focusing heavily on capacity expansion, renewable energy, and logistics optimization.

The management noted that with the successful integration of digital operations, power cost savings, and strategic logistics, Ambuja has significantly improved its operating margins while maintaining volume growth momentum.

The company reiterated its target to achieve 155 MTPA (Million Tonnes Per Annum) cement production capacity by FY28, up from the earlier target of 140 MTPA.

Operational Highlights

- Highest-Ever Quarterly Volumes:

Ambuja achieved record cement dispatches of 16.6 million tonnes during Q2 FY26, compared to 13.8 million tonnes in the same quarter last year. - Cost Optimization:

Fuel and power costs declined significantly due to the company’s focus on green energy and improved kiln efficiency. Lower logistics costs also contributed to margin expansion. - Green Power and Sustainability:

- Total renewable energy capacity stood at 673 MW by the end of Q2 FY26.

- The company aims to expand this to 900 MW by FY26-end and 1,122 MW by FY27, covering a significant portion of its total power requirement.

- Ambuja continues to prioritize its sustainability roadmap under the Adani Group’s green initiatives.

- Digital Transformation:

The company’s CINOC (Cement Intelligent Network Operations Centre), powered by AI and analytics, has optimized plant operations and real-time quality monitoring, reducing production downtime and improving throughput. - Expansion Projects:

- The Bhatapara (Chhattisgarh) new kiln line (4 MTPA) successfully began trial runs.

- The Krishnapatnam Grinding Unit (2 MTPA) is on track for commissioning in the next quarter.

- Additional 7 MTPA capacity is scheduled to come online during Q3 FY26.

Consolidated Financial Summary

| Parameter | Q2 FY26 | Q2 FY25 | Change |

|---|---|---|---|

| Revenue from Operations | ₹9,174 crore | ₹7,330 crore | +25% |

| EBITDA | ₹1,761 crore | ₹1,113 crore | +58% |

| Net Profit | ₹1,766 crore | ₹480 crore | +268% |

| EBITDA Margin | 19.2% | 15.1% | +4.1 pts |

| EPS | ₹7.2 | ₹2.0 | +267% |

| Sales Volume | 16.6 MnT | 13.8 MnT | +20% |

Segment Performance

Cement Segment:

The cement business recorded strong growth, supported by higher demand from infrastructure projects, rural housing, and improved dealer network expansion.

Ready-Mix Concrete (RMC) Segment:

The RMC division also registered steady performance with growth in urban markets.

Premium Product Mix:

Premium cement brands now contribute around 35% of Ambuja’s trade sales, helping the company maintain higher realizations and profitability.

More Articles You Might Find Useful:

- Q2 FY2025-26: Indian quarterly results 2025 Trend Report

- Netflix Announces 10-for-1 Stock Split: Here’s What Investors Need to Know

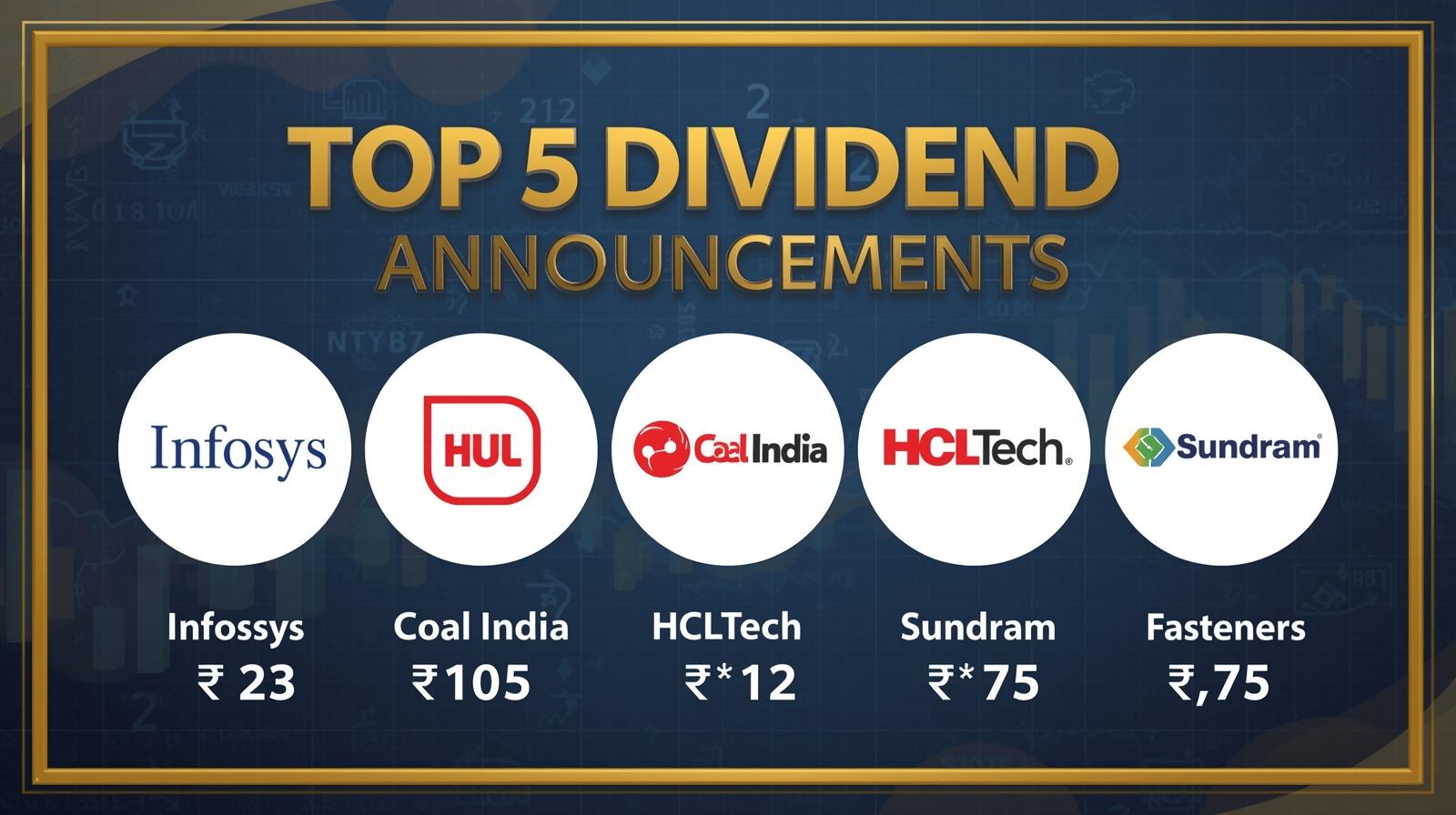

- Top 5 Dividend Announcements in India: Infosys, HUL, Coal India, HCL Tech, and Sundram Fasteners Reward Shareholders

- Reliance Jio–Google Partnership: 18-Month Free Gemini Pro Access Set to Boost AI Adoption in India

- Open Demat Account (M-Stock)

Factors Driving Performance

- Strong Cement Demand:

India’s ongoing infrastructure build-out, including highway, metro, and real estate projects, continues to fuel demand for cement. - Operational Efficiency:

Lower energy and logistics costs improved profitability. The company optimized its use of pet coke and alternative fuels, further reducing variable costs. - Sustainability Investments:

Ambuja’s continued focus on renewable energy and energy-efficient manufacturing supports both ESG goals and long-term cost competitiveness. - Adani Group Synergies:

Under the Adani Group, Ambuja benefits from logistics integration, renewable energy partnerships (Adani Green), and raw material sourcing efficiency.

Peer Comparison (Q2 FY26)

| Company | Revenue Growth | Net Profit Growth | EBITDA Margin | Debt Level |

|---|---|---|---|---|

| Ambuja Cements | +25% | +268% | 19.2% | Debt-free |

| UltraTech Cement | +12% | +32% | 18.7% | Moderate |

| ACC Ltd | +20% | +140% | 17.5% | Low debt |

| Shree Cement | +10% | +22% | 19.0% | Low debt |

Ambuja outperformed all its peers in profitability growth and margin expansion this quarter, reaffirming its leadership among India’s large-cap cement producers.

Balance Sheet Strength

Ambuja Cements continues to maintain a debt-free balance sheet with ample cash reserves, providing flexibility for future acquisitions and capital investments. The company’s net worth stood at ₹69,493 crore, up from ₹58,900 crore last year.

Strong internal accruals and minimal leverage ensure that Ambuja can comfortably fund its ambitious capacity expansion program without diluting shareholder value.

Expansion and Capacity Outlook

The company has revised its capacity expansion target to 155 MTPA by FY28, reflecting its aggressive growth plans under Adani Group leadership.

The roadmap includes:

- 4 MTPA expansion at Bhatapara, Chhattisgarh

- 2 MTPA grinding unit at Krishnapatnam

- 3 MTPA at a new facility in Maharashtra under planning

- Brownfield debottlenecking projects adding 6 MTPA cumulative capacity

These expansions will strengthen Ambuja’s presence in southern and eastern India — regions witnessing high infrastructure growth.

Sustainability and ESG Commitments

Ambuja Cements continues to strengthen its environmental stewardship.

Key ESG updates include:

- Increased use of alternative fuels and raw materials (AFR) to 12% of total energy mix.

- Reduction of CO₂ emissions per tonne of cement by 8% YoY.

- Increased share of renewable energy in total power consumption.

- Active projects under waste heat recovery systems (WHRS).

The company also reported that it aims for carbon neutrality by 2050, aligning with global cement industry standards.

Market Impact

After the Q2 results announcement, Ambuja Cements’ share price gained over 3% in early trading on NSE, touching ₹622 per share, reflecting investor confidence in the company’s growth trajectory.

Market analysts applauded the strong earnings, especially the margin expansion and debt-free position. Several brokerage firms upgraded Ambuja’s rating:

- HSBC: Upgraded to “Buy” with a revised target price of ₹700.

- Motilal Oswal: Maintained “Buy” rating with a target of ₹685.

- ICICI Securities: Reiterated “Add” rating, citing capacity growth and efficiency gains.

Investor Outlook

For retail and institutional investors, Ambuja Cements presents a compelling case:

- Growth Drivers: Capacity expansion, cost efficiency, and Adani synergy.

- Strong Fundamentals: Debt-free status, rising profitability, strong cash flow.

- Valuation: Trading at a forward P/E of around 27x FY26E earnings, still reasonable compared to sector peers.

- Dividend Potential: Strong free cash flow and zero debt leave room for consistent dividend payout.

Analysts expect Ambuja’s profit growth to continue at a compound annual rate (CAGR) of 20–25% over the next two years, supported by capacity additions and strong cement demand outlook.

Risks and Challenges

While the outlook remains strong, the company faces several sectoral risks:

- Input Cost Volatility: Coal and pet coke prices can fluctuate, impacting margins.

- Competition: Increasing capacity additions by peers could pressure pricing.

- Monsoon Dependency: Seasonal demand variations affect cement sales cycles.

- Regulatory and Environmental Compliance: Tightening emission norms may raise compliance costs.

Despite these factors, Ambuja’s strategic focus on renewable energy and efficiency positions it better than most competitors.

Adani Group Synergy

Being part of the Adani portfolio has provided Ambuja strategic advantages.

Key group-level synergies include:

- Adani Ports and Logistics: Ensures lower transportation and freight costs.

- Adani Green Energy: Supplies renewable power at competitive rates.

- Adani Enterprises (Resources arm): Enables secure and cost-efficient raw material sourcing.

These integrations have already started showing visible results in improved operating margins and sustainable growth.

Analyst Commentary

Industry experts view Ambuja’s performance as a signal of renewed strength in India’s cement sector.

- “Ambuja Cements’ 268% profit growth reflects Adani Group’s operational discipline and expansion momentum,” said an analyst at Jefferies India.

- “The company’s green power initiative and digitized operations set a new benchmark for cost efficiency in the cement industry,” noted Motilal Oswal Research.

- “We expect Ambuja’s volume CAGR to exceed 12% for FY26–27, backed by brownfield and greenfield expansions,” said Kotak Institutional Equities.

Long-Term Outlook

India’s cement demand is projected to grow at 8–9% annually for the next five years, supported by:

- Government focus on infrastructure

- Affordable housing projects

- Urbanization and industrial expansion

Ambuja’s position as a cost leader and its extensive distribution network ensure that it will remain one of the biggest beneficiaries of this growth wave.

By FY28, Ambuja and ACC together under Adani Cement are expected to surpass 150 MTPA — positioning the group as India’s largest cement producer, surpassing even UltraTech.

Conclusion

Ambuja Cements’ Q2 FY26 results underscore a remarkable turnaround story and growth momentum under the Adani Group. The company’s strong volume growth, improved margins, and sustainable energy push highlight its operational excellence and financial robustness.

With its ambitious expansion targets, focus on green energy, and digital transformation, Ambuja is poised to maintain leadership in India’s cement industry. For investors, Ambuja remains a solid long-term bet in the infrastructure growth story of India.

Open Demat Account

by Mirae Asset (m,Stock)

-

Trading Alert: Indian Stock Market Holidays on March 31 and Good Friday 2026

Stock Market Holidays 2026| NSE Holiday List| BSE Holidays| Mahavir Jayanti 2026| Good Friday 2026| Trading Calendar India| Share Market…

-

Nifty 50 and Sensex Post-Bloodbath Analysis: Recovery or Trap?

Nifty 50 Prediction Tomorrow| Sensex Analysis March 2026| Indian Stock Market Recovery| Stock Market Bloodbath Reasons The Indian stock market…

-

Stock Market Bloodbath 2026: 10 Rules to Protect Your Wealth

Stock Market Bloodbath 2026| Market Crash Strategy| Portfolio Recovery Tips| Investing in Volatile Markets Critical Event Status / Date Market…