Company Snapshot: Epigral Ltd

Epigral Ltd (formerly Meghmani Finechem Ltd) is a leading integrated chemical manufacturer based in Dahej, Gujarat. The company specializes in chlor-alkali, chloromethanes, epichlorohydrin, CPVC resin, and hydrogen peroxide—critical to sectors like pharmaceuticals, textiles, plastics, and agrochemicals.

| 🔹 Key Details | 🔹 Stats |

|---|---|

| Stock Symbol | NSE: EPIGRAL |

| Market Cap | ~₹7,900 Cr |

| CMP (July 2025) | ₹1,850 |

| 52-Week High / Low | ₹2406.75 / ₹1481.10 |

| P/E Ratio | ~22.6 |

| Dividend (FY25) | ₹6 per share |

📈 FY25: Revenue Breakout and Profit Surge

Epigral Ltd delivered a stellar performance in FY25, driven by both volume growth and margin expansion.

🧾 Consolidated Financials – FY25 (YoY)

-

Total Revenue: ₹2,565.3 Cr (vs ₹1,935.7 Cr in FY24) ↑ 32.5%

-

EBITDA: ₹725.9 Cr ↑ 49%

-

PAT: ₹357.7 Cr (vs ₹195.8 Cr) ↑ 82.6%

-

EPS: ₹93.71

-

Net Debt / EBITDA: Improved to 0.7× from 2.0×

This marks Epigral’s highest-ever earnings, powered by enhanced production across CPVC and epichlorohydrin segments.

📊 Q4 FY25 Snapshot: Seasonal Dip, But Strong Year

Though full-year numbers were robust, Q4 FY25 saw a modest decline from Q3:

| Metric | Q4 FY25 | Q4 FY24 | YoY Change |

|---|---|---|---|

| Revenue | ₹627 Cr | ₹526 Cr | ↑ 19.2% |

| PAT | ₹86.9 Cr | ₹77.3 Cr | ↑ 12.4% |

| EBITDA Margin | ~25% | ~22% | ↑ 300bps |

🔻 Quarterly fall: QoQ profit slipped ~16%, but analysts attribute this to seasonal fluctuations in chemical demand.

🔍 Business Mix: High-Margin Products Taking Lead

Epigral’s product portfolio transformation is helping it move up the value chain:

-

High-Value Products (HVP) contributed ~56% of revenue vs 25% in FY22.

-

First Indian company to produce bio-based epichlorohydrin using renewable glycerine.

-

Increased domestic demand for CPVC and H₂O₂ improved both volume and pricing power.

This import-substitution strategy gives Epigral a pricing moat in the Indian market.

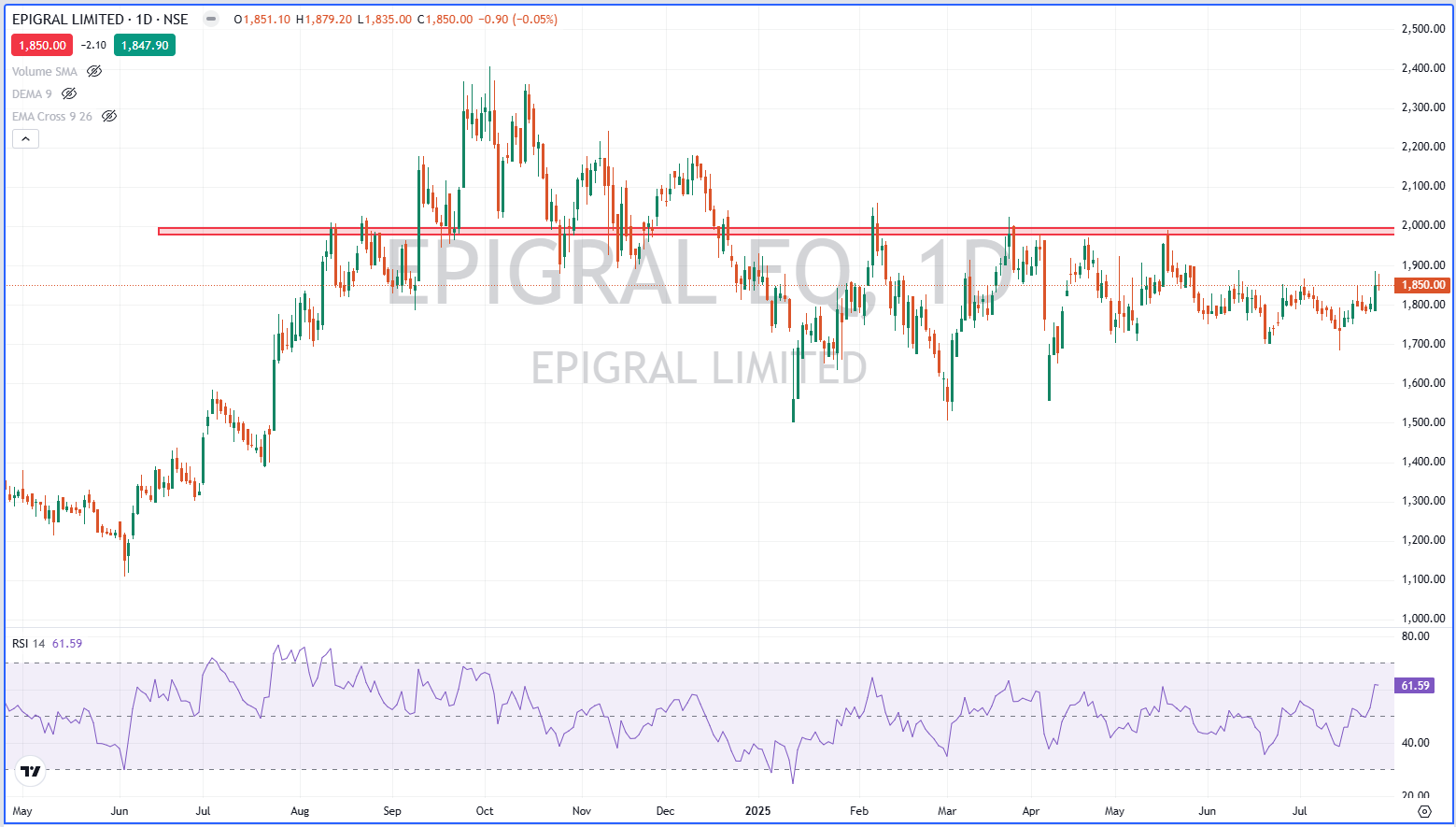

📉 Epigral Ltd Share Price Trend

📍 Technical Overview (as of July 27, 2025)

-

Current Price: ₹1,850

-

200-DMA: ₹1,720 (bullish crossover)

-

MACD: Positive crossover on daily chart

-

RSI: 58 (Neutral zone; no overbought signal yet)

📌 Watch for breakout above ₹1,900 for short-term momentum.

💰 Capital Strategy: Smart Debt Repayment

In FY25, Epigral:

-

Raised ₹333 Cr via QIP (₹2,093 per share)

-

Used ₹250 Cr to repay debt

-

Improved credit rating to AA (Stable) by CRISIL

-

ROCE jumped to 25%, up from 18% in FY24

💡 This balance sheet cleanup enhances long-term sustainability and reduces risk for investors.

🧭 Future Outlook: Expansion & Renewable Push

🔄 Upcoming Drivers

-

38 MW Hybrid Solar-Wind Plant (to be commissioned FY26)

-

Capacity addition in CPVC and chlorinated solvents

-

Targeting 20–25% revenue CAGR through FY27

📈 Retail Investor Relevance

-

Strong ROCE + low debt = capital-efficient growth

-

Dividend payout reflects shareholder alignment

-

Government push for Make in India + import bans in CPVC boost long-term demand

🧾 Dividend & Shareholder Return

| 🏷️ Final Dividend FY25 | ₹3.50 |

|---|---|

| Interim Dividend FY25 | ₹2.50 |

| Total FY25 Dividend | ₹6.00 |

| Dividend Yield | ~0.32% |

💬 Though yield is modest, capital appreciation potential is high.

📌 Conclusion: Why Epigral Is Worth Watching

✅ Financially stronger,

✅ Product-wise diversified,

✅ Strategically positioned for growth in import-substitute chemicals and green manufacturing.

🔎 Retail investors should track upcoming capacity expansions and monitor whether FY26 sees similar growth without margin pressure.

📉 Stock Market Disclaimer

Disclaimer: This post is for informational and educational purposes only and does not constitute financial advice or a recommendation to buy/sell any stock or share. Investing in the stock market involves risk. Past performance is not indicative of future results. Always conduct your own research or consult a licensed financial advisor before making investment decisions.